從債券形式來看,中國發行的國債可分為憑證式國債、無記名(實物)國債和記賬式國債三種。

憑證式國債是一種國家儲蓄債,可記名、掛失,以“憑證式國債收款憑證”記錄債權,不能上市流通,從購買之日起計息。在持有期內,持券人如遇特殊 情況需要提取現金,可以到購買網點提前兌取。提前兌取時,除償還本金外,利息按實際持有天數及相應的利率檔次計算,經辦機構按兌付本金的2‰收取手續費。

無記名(實物)國債是一種實物債券,以事物券的形式記錄債權,面值不等,不記名,不掛失,可上市流通。發行期內,投資者可直接在銷售國債機構的 櫃臺購買。在證券交易所設立賬戶的投資者,可委托證券公司通過交易系統申購。發行期結束後,實物券持有者可在櫃臺賣出,也可將實物券交證券交易所托管,再 通過交易系統賣出。

記賬式國債以記賬形式記錄債權,通過證券交易所的交易系統發行和交易,可以記名、掛失。投資者進行記賬式證券買賣,必須在證券交易所設立賬戶。由於記賬式國債的發行和交易均無紙化,所以效率高,成本低,交易安全。

Showing posts with label Treasuries. Show all posts

Showing posts with label Treasuries. Show all posts

Tuesday, September 27, 2016

引: (學習文) 美國公債

美國公債是美國財政部通過公債局發行的政府債券,屬貨幣市場工具,大致可分為四大種類:

1.U.S. Treasury bill叫作美國國庫券,英文簡稱T-bill,為美國政府發行的短天期債券,到期天數分別為4週,13週及26週、52週,每週拍賣一次。

2.U.S. Treasury Note稱為美國國庫票據,英文簡稱T-Note,發行期限在十年內,可分為2年、3年、5年、7年,2年期T-Note每月拍賣一次;3年期T-Note每季進行一次拍賣,分別在2、5、8、11月;5年期T-Note每月拍賣一次;10年期T-Note一年拍賣八次,分別在2、3、5、6、8、9、11及12月。

3.U.S. Treasury Bonds,英文簡稱T-Bonds,發行期限在十年以上,年限有10年、20年、30年。2002年二月曾經停止30年期國庫長期債券的發行,2006年二月又重新發行。

4.Treasury Inflation Protected Securities稱為美國國庫抗通膨債券,英文簡稱TIPS,1997年1月15日首次發行,本金具有隨通貨膨脹或緊縮作調整的特性,有三種到期天數,分別為5年、10年及20年。

2011年就在全球關注歐債的同時,美債違約危機警報大響。事實上,自1960年來,美國國會已採取了78次永久性的提高、暫時延長或修改定義債務上限,平均每八個月提高一次,其中共和黨及民主黨總統執政時期次數分別為49次和29次,2011年7月31日美國總統歐巴馬宣布兩黨對於提高美債上限達成協定,總計已採取了79次提高債務上限政策。

根據美國財政部公布的數據顯示,2011年5月突破的14.34兆美元的債務總額中,國內外投資者持有金額約9.74兆美元,通稱為公共持有債務,其餘的4.6兆美元則由美國政府管理的社會保險及信託基金持有。數據顯示9.74兆美元公共債務內,主要國家債權人持有美國國債總額達45140億美元,其中大陸持有金額達11598億美元,依然為持有美債第一大國。

據美國財政部定義,債務上限是指美國政府根據國會授權,用於履行現有法律規定義務,包括社會保險、醫療保險福利、軍事支出、國債利息、退稅及其他支出而產生的債務總額。

全文網址: http://www.moneydj.com/KMDJ/wiki/wikiViewer.aspx?keyid=809be277-f8b8-45ea-b96e-5f8beaff1feb#ixzz4LNVi9LD8

MoneyDJ 財經知識庫

債息簡介:

數據資料:

US Department of the Treasury

延伸:

詳細說明債券運作及其相關用辭以及投資債券方法 - Schroders

1.U.S. Treasury bill叫作美國國庫券,英文簡稱T-bill,為美國政府發行的短天期債券,到期天數分別為4週,13週及26週、52週,每週拍賣一次。

2.U.S. Treasury Note稱為美國國庫票據,英文簡稱T-Note,發行期限在十年內,可分為2年、3年、5年、7年,2年期T-Note每月拍賣一次;3年期T-Note每季進行一次拍賣,分別在2、5、8、11月;5年期T-Note每月拍賣一次;10年期T-Note一年拍賣八次,分別在2、3、5、6、8、9、11及12月。

3.U.S. Treasury Bonds,英文簡稱T-Bonds,發行期限在十年以上,年限有10年、20年、30年。2002年二月曾經停止30年期國庫長期債券的發行,2006年二月又重新發行。

4.Treasury Inflation Protected Securities稱為美國國庫抗通膨債券,英文簡稱TIPS,1997年1月15日首次發行,本金具有隨通貨膨脹或緊縮作調整的特性,有三種到期天數,分別為5年、10年及20年。

2011年就在全球關注歐債的同時,美債違約危機警報大響。事實上,自1960年來,美國國會已採取了78次永久性的提高、暫時延長或修改定義債務上限,平均每八個月提高一次,其中共和黨及民主黨總統執政時期次數分別為49次和29次,2011年7月31日美國總統歐巴馬宣布兩黨對於提高美債上限達成協定,總計已採取了79次提高債務上限政策。

根據美國財政部公布的數據顯示,2011年5月突破的14.34兆美元的債務總額中,國內外投資者持有金額約9.74兆美元,通稱為公共持有債務,其餘的4.6兆美元則由美國政府管理的社會保險及信託基金持有。數據顯示9.74兆美元公共債務內,主要國家債權人持有美國國債總額達45140億美元,其中大陸持有金額達11598億美元,依然為持有美債第一大國。

據美國財政部定義,債務上限是指美國政府根據國會授權,用於履行現有法律規定義務,包括社會保險、醫療保險福利、軍事支出、國債利息、退稅及其他支出而產生的債務總額。

全文網址: http://www.moneydj.com/KMDJ/wiki/wikiViewer.aspx?keyid=809be277-f8b8-45ea-b96e-5f8beaff1feb#ixzz4LNVi9LD8

MoneyDJ 財經知識庫

債息簡介:

票息如何釐定?取決於數項考慮因素:

- 到期日越遠,利率越高

一般來說,當鎖定資金的時間越長,投資者要求的利率越高。 - 風險越高,利率越高

這是因為投資者會按他承擔的風險而要求相稱的補償。 - 通脹越高,利率越高

為防止通脹蠶食利潤,投資者會把通脹溢價計入他要求的利率內。

以下是常用的債券詞語﹕

| 詞語 | 解釋 | 例子 |

| 面值 | 貸款本金 | $10,000 |

| 票息 | 按面值及預定利率而支付的利息 | 年息 10% |

| 孳息率 | 債券票息除以債券市價 | 債券市價< 100,孳息率> 10% 債券市價> 100,孳息率< 10% |

| 到期日 | 預定的貸款償還日期 | 由今天起計10年後 |

數據資料:

US Department of the Treasury

延伸:

詳細說明債券運作及其相關用辭以及投資債券方法 - Schroders

Monday, September 26, 2016

引: U.S. Bond Market’s Biggest Buyers Are Selling Like Never Before

U.S. Bond Market’s Biggest Buyers Are Selling Like Never Before

- Central banks have cut Treasuries for three straight quarters

- Pullback may be a sign the bond market is at a tipping point

They’ve long been one of the most reliable sources of demand for U.S. government debt.

But these days, foreign central banks have become yet another worry for investors in the world’s most important bond market.

Holders like China and Japan have culled their stakes in Treasuries for three consecutive quarters, the most sustained pullback on record, based on the Federal Reserve’s official custodial holdings. The decline has accelerated in the past three months, coinciding with the recent backup in U.S. bond yields.

For Jim Leaviss at M&G Investments in London, that’s cause for concern. A continued retreat could lead to painful losses in a market that some say is already too expensive. But perhaps more important are the consequences for America’s finances. With the U.S. facing deficits that are poised to swell the public debt burden by $10 trillion over the next decade, foreign demand will be crucial in keeping a lid on borrowing costs, especially as the Fed continues to suggest higher interest rates are on the horizon.

The selling pressure from central banks is “something you have to bear in mind,” said Leaviss, whose firm oversees about $374 billion. “This, as well as the Fed, all means we are nearer to the end of the low-yield environment.”

To shield his clients from higher yields, Leaviss said M&G has scaled back on longer-term Treasuries and favors shorter-maturity securities.

Overseas creditors have played a key role in financing America’s debt as the U.S. borrowed heavily in the aftermath of the financial crisis to revive the economy. Since 2008, foreigners have more than doubled their investments in Treasuries and now own about $6.25 trillion.

Central banks have led the way. China, the biggest foreign holder of Treasuries, funneled hundreds of billions of dollars back into the U.S. as its export-based economy boomed.

Now, that’s all starting to change. The amount of U.S. government debt held in custody at the Fed has decreased by $78 billion this quarter, following a decline of almost $100 billion over the first six months of the year. The drop is the biggest on a year-to-date basis since at least 2002 and quadruple the amount of any full year on record, Fed data show.

The custodial data add to evidence that the retreat isn’t simply a one-off. Separate figures from the Treasury Department showed that China pared its stake to $1.22 trillion in July, the lowest level in more than three years. Others, like Japan and Saudi Arabia, have also reduced their holdings this year.

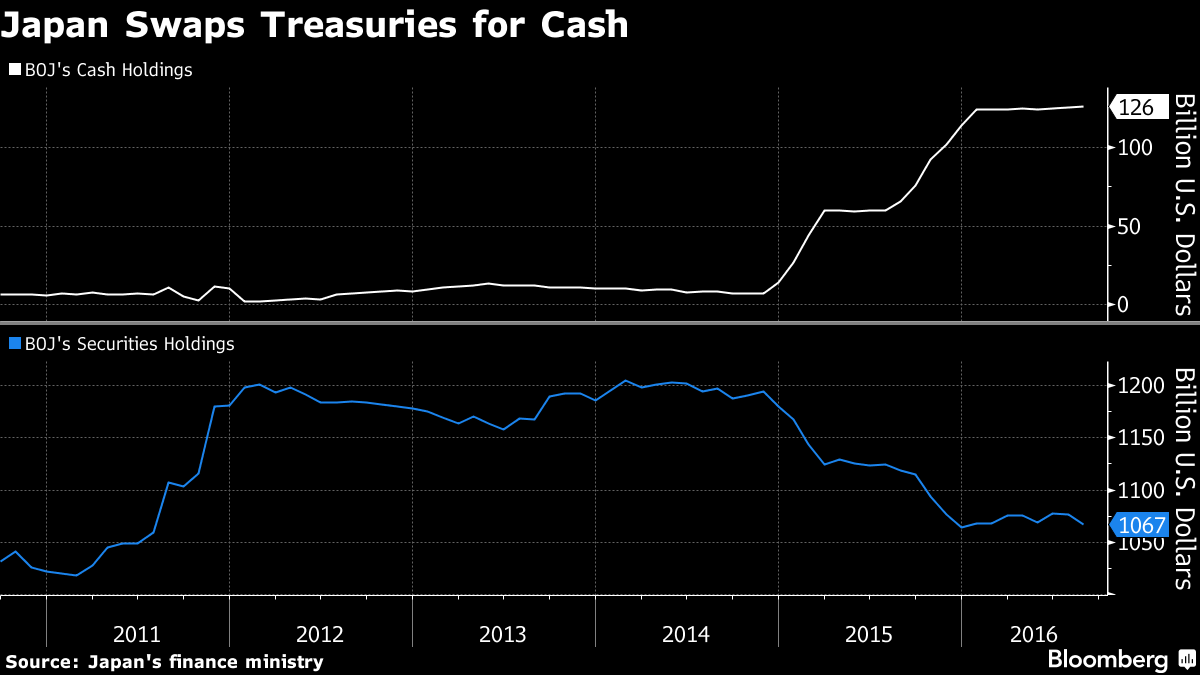

Big holders of Treasuries are selling for a variety of reasons, but they’re all tied to each country’s economic woes. In China, the central bank has been selling U.S. government debt to defend the yuan as slumping growth leads to more capital outflows. Japan, the second-biggest foreign holder, has swapped Treasuries for cash and T-bills as prolonged negative rates in the Asian nation pushed up dollar demand at local banks.

Oil-producing countries like Saudi Arabia have been liquidating Treasuries to plug their budget deficits following the collapse of crude prices. Saudi Arabia’s holdings have declined for six straight months to $96.5 billion -- the lowest since November 2014.

“Their trade position is markedly worse” because of the slump in oil, said Peter Jolly, the head of market research at National Australia Bank Ltd. That means “their need to purchase Treasuries is greatly reduced.”

The decline in central bank demand -- which some models show has cut 10-year Treasury yields by an extra 0.4 percentage point -- points to one reason that U.S. borrowing costs may finally be on the upswing after they fell to a record-low 1.318 percent in July.

What’s more, some measures suggest Treasuries aren’t providing any margin of safety.

While yields have risen to 1.6 percent, that’s still leaves many overseas investors vulnerable. For yen- and euro-based buyers who hedge out the dollar’s fluctuations -- a common practice among insurers and pension funds -- yields are effectively negative. Meanwhile, a valuation tool called the term premium stands at minus 0.58 percentage point for 10-year notes. In the previous 50 years, it has almost always been positive.

Despite those warnings, the bulls say things like tepid U.S. growth and $10 trillion of negative-yielding government debt will keep Treasuries in demand.

“It’s still attractive of course,” said Hideo Shimomura, the chief fund investor at Mitsubishi UFJ Kokusai Asset Management, which oversees about $118 billion. “People might begin to chase yields again.”

Homegrown demand has helped pick up the slack. Excluding short-term bills, U.S. money managers have snapped up 45 percent of the $1.1 trillion in Treasuries sold at government auctions this year, the highest share since the Treasury began breaking out the data six years ago. In 2011, it was as low as 18 percent. U.S. commercial banks, for their part, have also added to their investments of government debt, boosting stakes to a record $2.38 trillion at the end of August.

Nevertheless, some of the most influential players say in the market it’s time to get defensive. Last week, DoubleLine Capital’s Jeffrey Gundlach predicted that benchmark Treasury yields will exceed 2 percent before year-end, echoing his earlier call that the bond market had finally reached a tipping point. At the same time, the Fed signaled at its September meeting that it’s likely to lift rates by December.

For central banks, “why wouldn’t they reduce their Treasury holdings?” said Mark Holman, the chief executive officer at Twentyfour Asset Management, which oversees $9.8 billion. “There is yield available there, but you have a Fed that’s been reasonably clear in what it wants to do -- it’s looking to hike.”

Whatever the case, there’s little doubt that America’s borrowing needs will only grow with time -- and that could add up to hundreds of billions of dollars in additional interest if foreign demand doesn’t hold up.

The Congressional Budget Office forecasts the U.S. deficit will rise to $590 billion in the fiscal year ending Sept. 30, the first annual increase since 2011. Over the next decade, successive shortfalls to cover costs for Medicare and Social Security will cause the public debt burden to balloon to $23 trillion.

“It’s just the beginning,” said Park Sung-jin, the head of principal investment at Mirae Asset Securities Co., which oversees $8 billion.

=====

- Central banks have cut Treasuries for three straight quarters

- Pullback may be a sign the bond market is at a tipping point

They’ve long been one of the most reliable sources of demand for U.S. government debt.

But these days, foreign central banks have become yet another worry for investors in the world’s most important bond market.

Holders like China and Japan have culled their stakes in Treasuries for three consecutive quarters, the most sustained pullback on record, based on the Federal Reserve’s official custodial holdings. The decline has accelerated in the past three months, coinciding with the recent backup in U.S. bond yields.

For Jim Leaviss at M&G Investments in London, that’s cause for concern. A continued retreat could lead to painful losses in a market that some say is already too expensive. But perhaps more important are the consequences for America’s finances. With the U.S. facing deficits that are poised to swell the public debt burden by $10 trillion over the next decade, foreign demand will be crucial in keeping a lid on borrowing costs, especially as the Fed continues to suggest higher interest rates are on the horizon.

The selling pressure from central banks is “something you have to bear in mind,” said Leaviss, whose firm oversees about $374 billion. “This, as well as the Fed, all means we are nearer to the end of the low-yield environment.”

To shield his clients from higher yields, Leaviss said M&G has scaled back on longer-term Treasuries and favors shorter-maturity securities.

Overseas creditors have played a key role in financing America’s debt as the U.S. borrowed heavily in the aftermath of the financial crisis to revive the economy. Since 2008, foreigners have more than doubled their investments in Treasuries and now own about $6.25 trillion.

Central banks have led the way. China, the biggest foreign holder of Treasuries, funneled hundreds of billions of dollars back into the U.S. as its export-based economy boomed.

Now, that’s all starting to change. The amount of U.S. government debt held in custody at the Fed has decreased by $78 billion this quarter, following a decline of almost $100 billion over the first six months of the year. The drop is the biggest on a year-to-date basis since at least 2002 and quadruple the amount of any full year on record, Fed data show.

The custodial data add to evidence that the retreat isn’t simply a one-off. Separate figures from the Treasury Department showed that China pared its stake to $1.22 trillion in July, the lowest level in more than three years. Others, like Japan and Saudi Arabia, have also reduced their holdings this year.

Big holders of Treasuries are selling for a variety of reasons, but they’re all tied to each country’s economic woes. In China, the central bank has been selling U.S. government debt to defend the yuan as slumping growth leads to more capital outflows. Japan, the second-biggest foreign holder, has swapped Treasuries for cash and T-bills as prolonged negative rates in the Asian nation pushed up dollar demand at local banks.

Oil-producing countries like Saudi Arabia have been liquidating Treasuries to plug their budget deficits following the collapse of crude prices. Saudi Arabia’s holdings have declined for six straight months to $96.5 billion -- the lowest since November 2014.

“Their trade position is markedly worse” because of the slump in oil, said Peter Jolly, the head of market research at National Australia Bank Ltd. That means “their need to purchase Treasuries is greatly reduced.”

The decline in central bank demand -- which some models show has cut 10-year Treasury yields by an extra 0.4 percentage point -- points to one reason that U.S. borrowing costs may finally be on the upswing after they fell to a record-low 1.318 percent in July.

What’s more, some measures suggest Treasuries aren’t providing any margin of safety.

While yields have risen to 1.6 percent, that’s still leaves many overseas investors vulnerable. For yen- and euro-based buyers who hedge out the dollar’s fluctuations -- a common practice among insurers and pension funds -- yields are effectively negative. Meanwhile, a valuation tool called the term premium stands at minus 0.58 percentage point for 10-year notes. In the previous 50 years, it has almost always been positive.

Despite those warnings, the bulls say things like tepid U.S. growth and $10 trillion of negative-yielding government debt will keep Treasuries in demand.

“It’s still attractive of course,” said Hideo Shimomura, the chief fund investor at Mitsubishi UFJ Kokusai Asset Management, which oversees about $118 billion. “People might begin to chase yields again.”

Homegrown demand has helped pick up the slack. Excluding short-term bills, U.S. money managers have snapped up 45 percent of the $1.1 trillion in Treasuries sold at government auctions this year, the highest share since the Treasury began breaking out the data six years ago. In 2011, it was as low as 18 percent. U.S. commercial banks, for their part, have also added to their investments of government debt, boosting stakes to a record $2.38 trillion at the end of August.

Nevertheless, some of the most influential players say in the market it’s time to get defensive. Last week, DoubleLine Capital’s Jeffrey Gundlach predicted that benchmark Treasury yields will exceed 2 percent before year-end, echoing his earlier call that the bond market had finally reached a tipping point. At the same time, the Fed signaled at its September meeting that it’s likely to lift rates by December.

For central banks, “why wouldn’t they reduce their Treasury holdings?” said Mark Holman, the chief executive officer at Twentyfour Asset Management, which oversees $9.8 billion. “There is yield available there, but you have a Fed that’s been reasonably clear in what it wants to do -- it’s looking to hike.”

Whatever the case, there’s little doubt that America’s borrowing needs will only grow with time -- and that could add up to hundreds of billions of dollars in additional interest if foreign demand doesn’t hold up.

The Congressional Budget Office forecasts the U.S. deficit will rise to $590 billion in the fiscal year ending Sept. 30, the first annual increase since 2011. Over the next decade, successive shortfalls to cover costs for Medicare and Social Security will cause the public debt burden to balloon to $23 trillion.

“It’s just the beginning,” said Park Sung-jin, the head of principal investment at Mirae Asset Securities Co., which oversees $8 billion.

=====

聯儲局為外國央行代為持有的美國國債總額,在第三季減少780億美元,而今年上半年亦錄得1000億減少,這下跌幅度為超碼是2002年以來最大。

這個跌幅相信與中國、沙特阿拉伯及日本央行顯著減持美國國債持債量有關。

Subscribe to:

Posts (Atom)